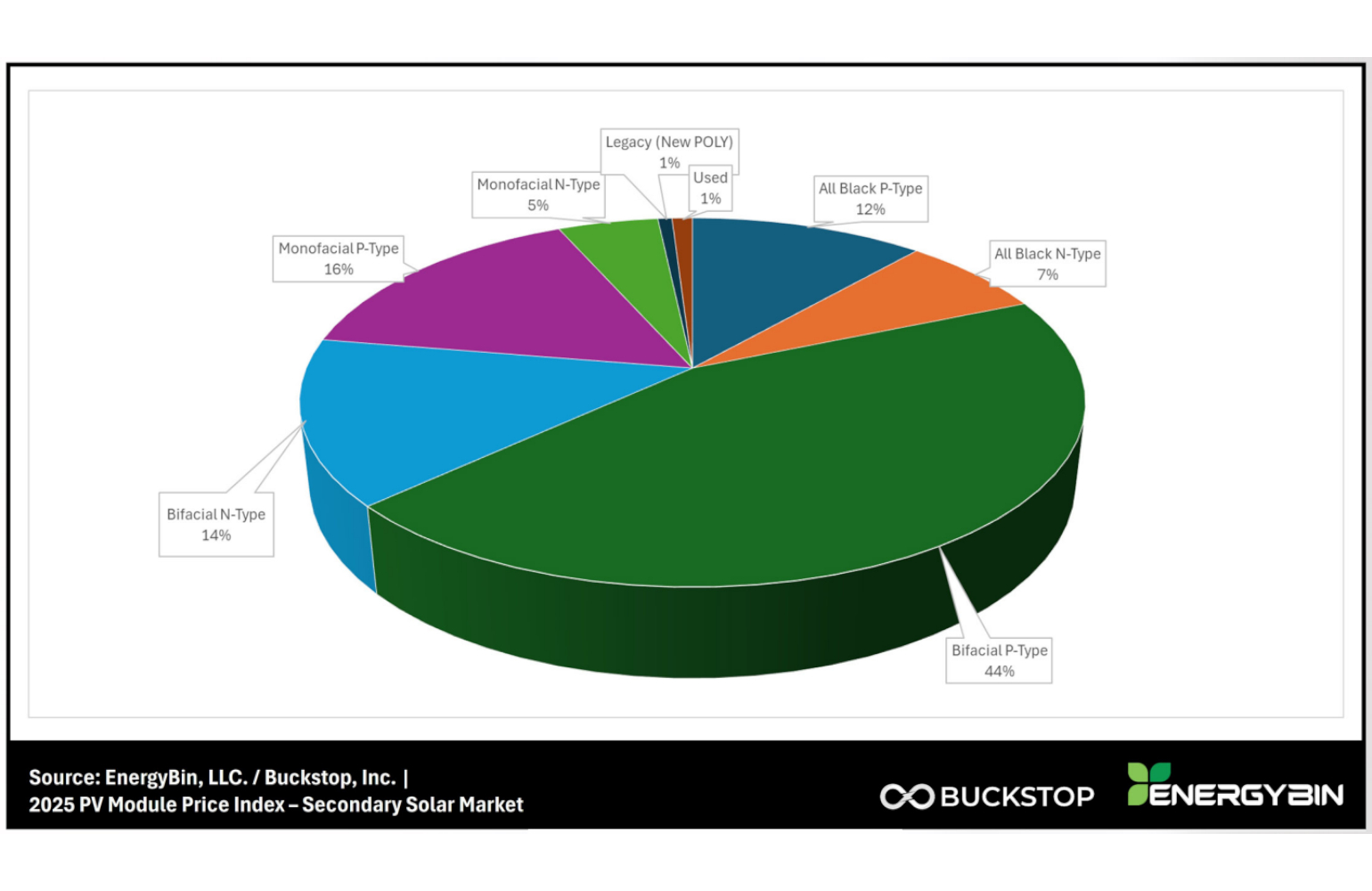

The fifth annual “PV Module Price Index – Secondary Solar Market” report from EnergyBin and Buckstop shows that 98% of solar panels in the secondary market are in the 400 to 525 W range and most appropriate for the residential market.

The price index tracks wholesale pricing and supply of crystalline-silicon (c-Si) modules that have fallen out of traditional distribution channels, and as a result are listed for resale on the EnergyBin exchange. As a B2B wholesale solar equipment exchange comprised of over 1,000 member companies, EnergyBin facilitates the connection of solar companies looking to buy and sell PV hardware. Although transactions do not take place on the EnergyBin platform, sales listings documented more than 8.7 million modules posted to the site for resale from January 2020 through December 2025.

“For the fifth year in a row, the PV Module Price Index has provided evidence that points to a growing secondary solar market,” says Renee Kuehl, COO at EnergyBin. “What’s clear from this price index is that most remarketed modules retain resale value. Even as global prices fell since 2023, the price index highlights some level of incubation within the U.S. market.”

In 2025, modules listed for resale were predominantly new (98%) all-black, bifacial and monofacial types with a power range from 400 to 525 W. This volume primarily flowed from project cancelations and delays. Additionally, a rush to offload p-type modules increased secondary market supply as resellers anticipate PERC production phase-outs. The resale value for PERC modules held steady throughout the year but will begin to slide as n-type supply overtakes p-type.

Another key finding revealed the effect of global oversupply upon used module resale. The average price for used modules plummeted by 30% from January 2024, down to $0.058/W in Q4 2025. With new TOPCon modules listed at $0.090/W shipped FOB from China (as of December), the case for resale was somewhat hampered. However, a market size analysis provided by Buckstop indicated that much of the used module supply bypassed wholesale exchanges, like EnergyBin, and exported directly to buyers in other countries, including Pakistan, India, Nigeria, Afghanistan and South Africa. In 2025, U.S. used module exports to these countries totaled 50 MW.

One exception that appears to justify the viability of used module resale today is that of top-quality modules, which are less than 10 years old, report a degradation rate of at or below 0.5-1% per year, and are defect-free. As buyers favor well-made modules over price, used module resale, particular those in excellent working condition with 3.2-mm glass and no cracked backsheets, becomes an opportunity.

“The secondary market offers solar companies the opportunity to create financial, social, and operating value,” says Nick Kumleben, chief business development officer and co-founder at Buckstop. “Secondary markets are not just useful sources for spare parts and liquidity sources for excess stock. Resale also allows solar operators to find used parts, donate unwanted inventory, lessen supply chain shortages through recycling, and help solve energy poverty around the world.”

For the fifth year of publishing the report, the findings point to opportunities that lie within a robust and sustainable secondary market that supports the ongoing extension of PV asset lifecycles, maximization of asset recovery and minimization of solar e-waste. Both the value and size of the secondary market increase as reuse of PV modules not yet at end-of-life becomes mainstream and a comprehensive recycling infrastructure to extract and redeploy materials is established.

See results from the 2025 and 2024 reports.

{kind=link}