From Texas-sized utility projects to skyrocketing residential battery attach rates, 2026 marks the year solar and storage transition from the electric grid’s fastest-growing additions to its foundational pillars.

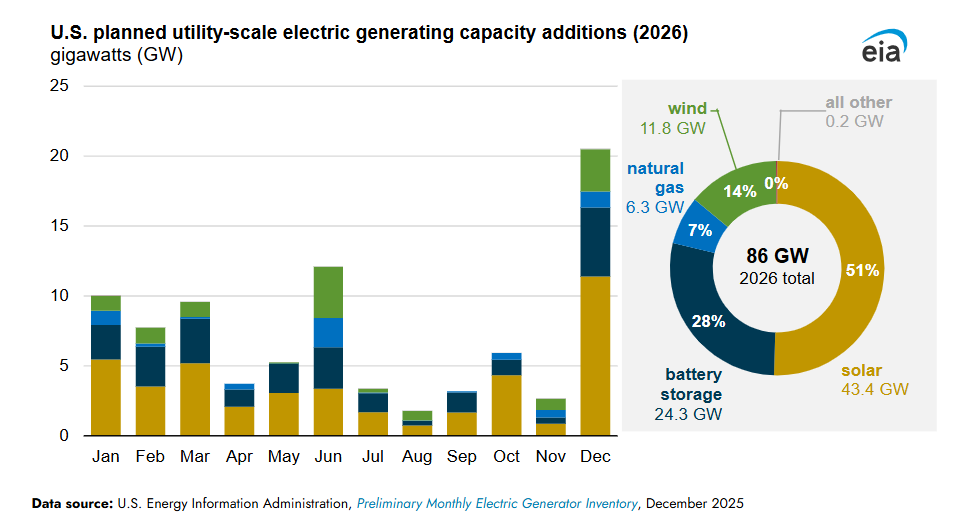

Project developers and utility operators are preparing for a historic expansion of the U.S. electric grid, with 86 GW of new utility-scale generating capacity slated to come online in 2026.

According to the February 2026 Electric Power Monthly report from the Energy Information Administration (EIA), the surge represents the largest single-year capacity addition in over two decades, nearly doubling the 53 GW installed in 2025.

The growth is overwhelmingly driven by “the big two” of the energy transition: solar and battery storage. Combined, these two technologies account for 79% of all planned additions for the year.

Solar’s 60% year-over-year growth

Solar power continues its run as the fastest-growing source of new generation. Developers plan to add 43.4 GW of utility-scale solar in 2026, a 60% increase over the record-setting 27.2 GW added in 2025. If the projects materialize as scheduled, 2026 will mark the third consecutive year of record solar installations.

Geographically, Texas remains the epicenter of the solar boom, hosting approximately 40% (17.4 GW) of the nation’s planned solar construction. Arizona and California follow, each accounting for roughly 6% of the national total.

Notable projects driving this trend include the Tehuacana Creek 1 Solar facility in Navarro County, Texas, which is expected to bring 837 MW of photovoltaic capacity online this year.

Battery energy storage has now entered center stage as as grid asset. The EIA expects 24.3 GW of new battery storage to come online in 2026, surpassing the 15 GW record set in 2025. This rapid scaling follows a five-year trend of exponential growth, with the U.S. now boasting over 40 GW of installed storage capacity.

Approximately 48% of current storage on the grid is co-located with solar arrays, a strategy designed to mitigate curtailment and shift peak production to meet evening demand. Major storage assets scheduled for 2026 commercial operation include the Lunis Creek BESS (621 MW) and the Clear Fork Creek Solar & BESS (600 MW), both in Texas.

Distributed solar

While utility-scale solar dominates the volume, the distributed, small-scale sector is undergoing a structural shift. Small-scale solar generation increased by roughly 11% year-over-year, now contributing 2.13% of total U.S. electrical generation. The focus in the sector has shifted from simple “panels on roofs” to more sophisticated integrated energy systems.

As states like California transition from 1:1 net metering to “Net Billing” structures, the value proposition for selling power back to the grid has diminished. This policy change is driving a massive spike in battery attachment rates with solar projects.

In California, the residential battery attachment rate has reached 69%. The trend is expected to go national, and by 2030, analysts project that one in eight American homes will have solar, with a vast majority opting for storage to maximize self-consumption and avoid lower utility buy-back rates.

In emerging markets like Colorado, matching California levels of attachment rates could unlock up to 2 GWh of new residential battery capacity by 2040, said the report.

The integration of distributed storage is also proving critical for seasonal grid stability. In New York, where distributed storage is projected to reach 3.7 GW by 2035, data shows that 56% of the energy cost savings from these systems occur during the winter months (November to March). This aligns with critical winter reliability needs, providing a buffer when fossil fuel plants often face operational stresses and failures.

Renewables vs. fossil fuels

Renewables and storage are projected to account for 93% of all new utility-scale capacity this year. In contrast, natural gas developers plan to add only 6.3 GW of new capacity.

With the 2026 additions, the EIA anticipates that solar generation specifically will grow from 290 TWh in 2025 to over 420 TWh by the end of the year. As the grid moves toward a mix where solar, wind, and storage dominate nearly all net-new capacity, the focus is now placed on how fast the infrastructure can be interconnected to the grid.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Popular content

{kind=link}